26

May

What the new tax year means for your money and inheritance

Sponsored

As we continue in the new tax year, those seeking to protect their wealth and their families’ futures can draw on plenty of old strategies but also face new challenges. S&W’s experts explore what you should be doing to make sure you don’t miss out.

Perhaps the biggest change for tax from April 2026 is for the self-employed and landlords. With the rollout of the Making Tax Digital programme for income tax, sole traders and landlords earning more than £50,000 a year now need to use software (or an accountant with their own) to submit quarterly updates of income and expenses to HMRC.

They won’t have to pay the tax any earlier than usual, but it’s a substantial new burden for many.

Key tax changes for 2026

For others, however, the new tax year has brought fewer changes – largely reflecting that the Chancellor’s Budget last November was less radical than her first in 2024. As a result, many of the strategies to minimise liabilities remain the same:

- Using your ISA tax-free savings allowance – and both allowances if you’re a couple. It’s the last year you’ll be able to put the full £20,000 in cash, as this is being limited to £12,000 in April 2027 for investors under the age of 65, with the remainder reserved for investment ISAs. Parents and grandparents, don’t forget children’s ISA allowances.

- Using your pension allowance (for most people £60,000 this tax year). Again, things change next year, with salary sacrifice on pension contributions limited to £2,000, so use it while you can. And again, for those looking to pass on wealth, consider putting money in junior SIPPs or the pensions of working-age children.

- For workers, pension contributions also remain a useful tool to avoid the 60% tax trap; marginal tax rates for those earning between £100,000 and £125,000 are punishing due to the withdrawal of personal tax allowances. If you can, you want to avoid your taxable income falling in that band.

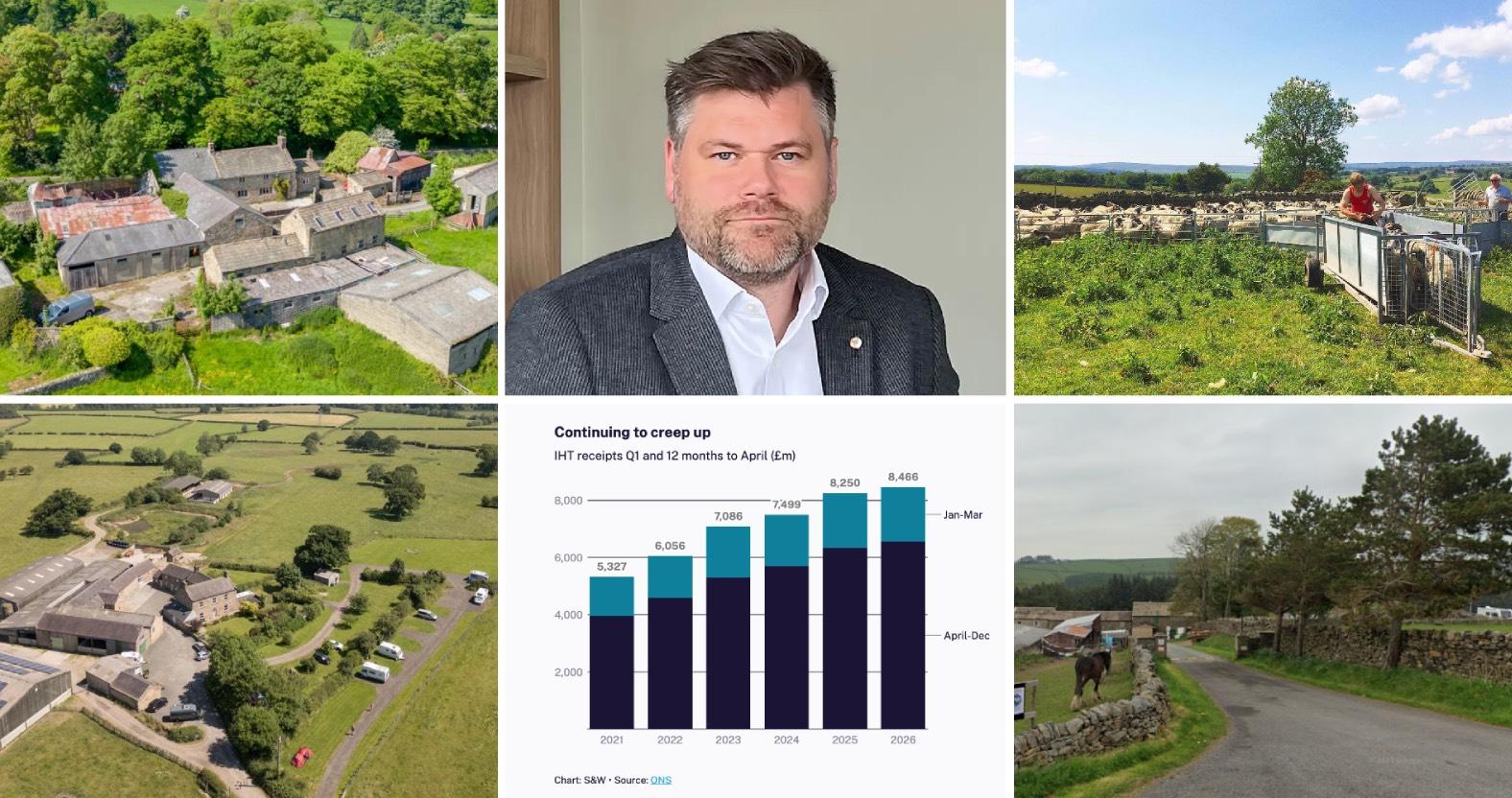

Examples of farms across the Harrogate district that will be affected by the new inheritance tax laws

New rules for inheritance tax

For farm and business owners, the biggest change from April is still probably the limiting of full business property and agricultural relief to the first £2.5 million of assets, or £5 million for a couple. Assets above that value get only half the relief, so pay 20% inheritance tax (IHT). April was also the cut-off to put assets into trusts to lock in the relief.

But that doesn’t mean there’s no longer any point in thinking about it.

First, trusts will continue to be popular – perhaps even more so now that you can’t simply rely on passing business and farm assets on tax free. Putting them in a trust starts the clock running for the seven-year rule (after which assets pass out of the estate for IHT purposes), while keeping some control.

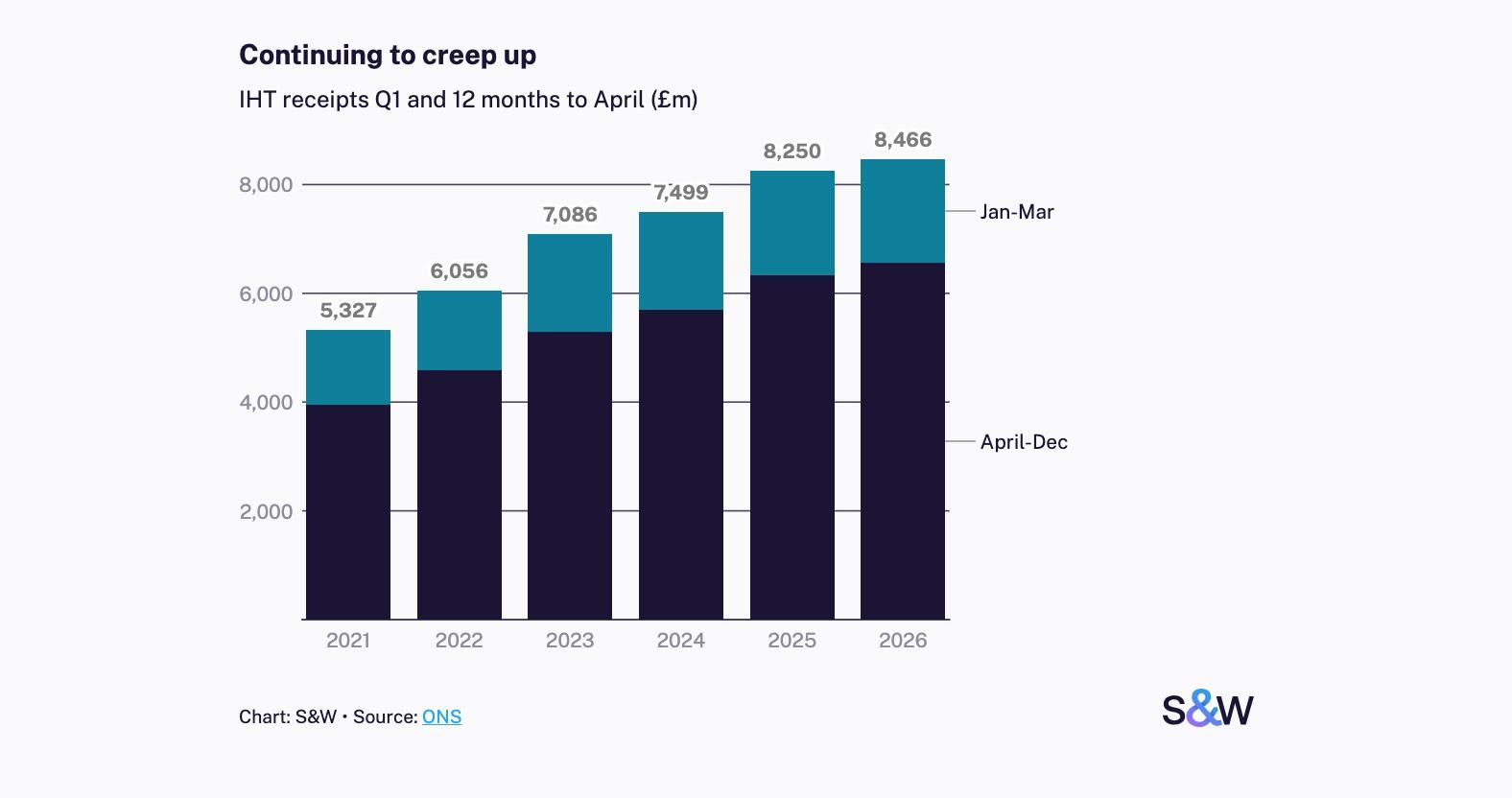

More fundamentally, everyone with substantial assets, business owner or otherwise, needs to regularly review their estate planning. Inheritance tax receipts in the 12 months to April hit a record £8.47 billion, and frozen allowances and rising asset prices mean that figure is only likely to grow.

Giving it away: minimising IHT

The seven-year rule for IHT and gifting assets is well understood, but it’s sometimes forgotten that the relief tapers: the IHT rate payable starts declining from three years after the assets are gifted or put into a trust. Consequently, if you plan to pass them on, it pays to start early.

Less well-known – or at least less used – is the allowance for normal expenditure out of excess income. For many, this can be hugely valuable, providing immediate relief, with assets leaving the estate without the seven-year delay. There’s no limit to how much you can give, provided that it should be regular gifts from income rather than capital, and that they don’t affect the giver’s standard of living.

For excess income from a job, business, pension, property, savings interest or investments, it’s an effective and tax-efficient way to pass on wealth free from IHT. If you’re uncertain about your future needs and giving a large lump sum, regular gifting can at least prevent unneeded income from further accumulating in the estate.

Be sure to take advice to avoid any potential pitfalls, but also be sure to act, reviewing your options and taking advantage of allowances and reliefs while they’re still there. Because the next new tax year will soon come around.

Partner in S&W’s Harrogate office, Stuart Wright

At S&W we’ve been helping clients protect and pass on their wealth since 1881. To discuss how we can help secure the future you want for yourself and your family, contact Stuart Wright, Partner in S&W’s Harrogate office: stuart.wright@swgroup.com or visit the website www.swgroup.com.

0